July Update

U.S. Equity Markets

U.S. equities experienced a month of mixed performance for July. The S&P 500 ended July with a modest gain of 1.5%, buoyed by strong earnings reports from major technology companies and renewed optimism over economic growth. However, the Nasdaq Composite showed more volatility, closing slightly lower by 0.7% due to concerns about regulatory scrutiny impacting the tech sector.

In July, U.S. tech giants demonstrated continued robust performance across various sectors. Major players like Apple, Microsoft, and Amazon reported strong earnings driven by advancements in cloud computing, digital services, and e-commerce. Companies like Alphabet and Meta benefited from substantial growth in advertising and emerging technologies. NVIDIA's results highlighted the increasing demand for AI-driven solutions, while Tesla's strong performance was underpinned by innovations in electric vehicles and energy solutions.

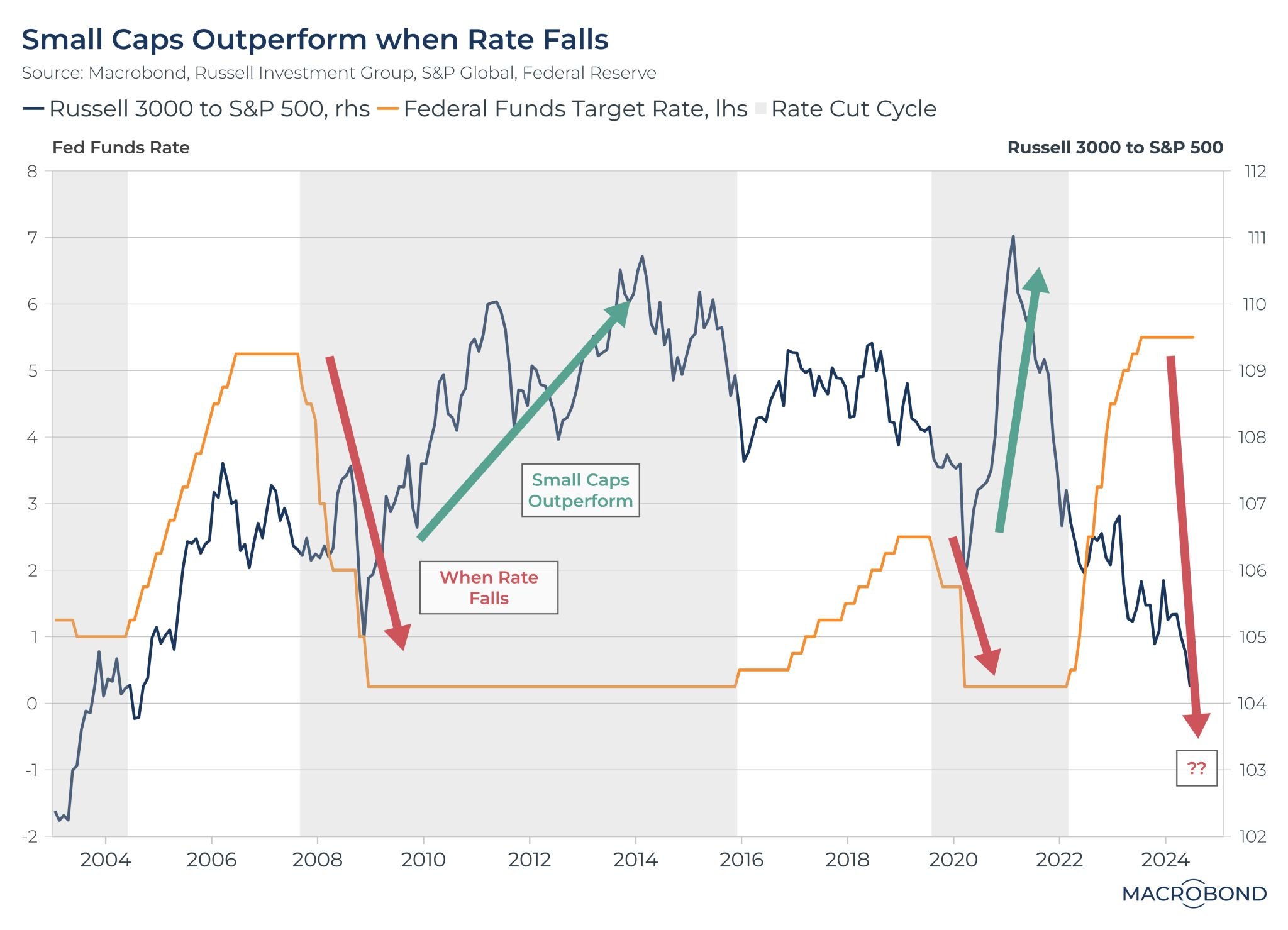

Rate falls, Small Caps calls?

With disinflation continuing and the labour market weakening, a rate cut should be on the horizon. Is it time to consider buying small caps?

Historically, Small Caps have outperformed when interest rates fall, dating back to the internet bubble era. This trend is intact when comparing the Russell 3000 to S&P 500 ratio against the Fed Funds Rate.

Source: Macrobond

Inflation and Employment Reports

The U.S. Labor Department released its July employment report, revealing an increase in the unemployment rate to 4.3% from 4.1% in June. This uptick was attributed to slower job growth compared to previous months. Additionally, inflation data showed a slight moderation in consumer price increases compared to previous months.

The increase in the unemployment rate raised concerns about a potential cooling in the labor market, while the moderating inflation figures provided some relief. These mixed signals contributed to a complex economic outlook, influencing both market sentiment and Federal Reserve expectations.

Employment rising

The U.S. labor market is showing further signs of cooling, with the unemployment rate rising to 4.4% from 4.3% in July. Nonfarm payrolls grew by 175,000, a slowdown from the previous month’s 220,000 new jobs. Notable gains were seen in healthcare and professional services, while sectors like retail and education experienced slower growth. The labor force participation rate held steady at 63.0%, and average hourly earnings rose by 0.3% from July, reflecting a year-over-year increase of 4.2%. Overall, the employment landscape remains stable but with slower job creation and a slight uptick in unemployment, signaling a gradual shift in the labor market.

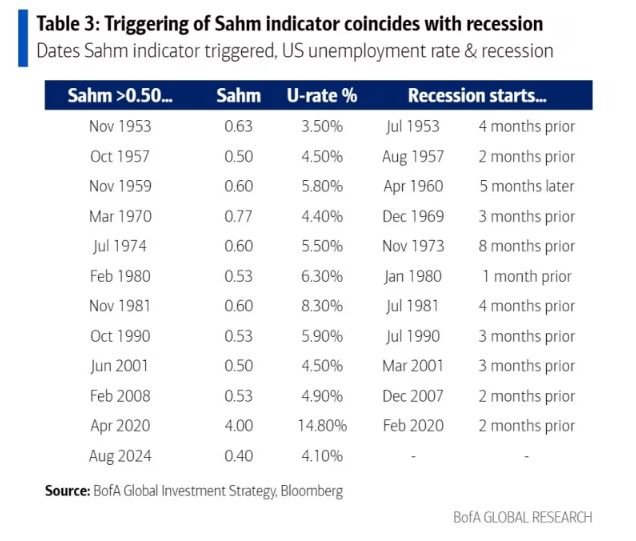

The Sahm Rule that is designed to signal the start of a recession has officially been triggered. The rule indicates a recession has started when the three-month moving average of the US unemployment rate is 0.5 percentage points or more above its lowest during the previous 12 months. Since 1953, the Sahm Rule has never been wrong. With the unemployment print ticking up in July, The Sahm Rule reading reached 0.53 points in July.

Source: BofA Global Research

Rate Cut Expectations Are Rising

Federal Reserve Chairman Nick Tamiraos of the Wall Street Journal says that the Federal Reserve is likely to cut rates three or more times in the second half of 2024. Most sell-side economists and other professional Fed watchers expect the Fed to cut interest rates by a quarter at each of its three remaining policy meetings this year. But now there is more deviation as a few give the possibility of larger declines.

Source: Wall Street Journal

Geopolitical Tensions and Oil Prices

In July 2024, the geopolitical tensions between Iran and Israel significantly escalated, impacting global oil markets with notable volatility. During this period, Israeli forces killed two key militant leaders: Imad Mughniyeh, a senior Hezbollah commander involved in various attacks against Israel, and Alaa al-Din al-Batsh, a senior Hamas military commander in Gaza. This escalation caused crude oil prices to surge by 3.4% as investors grew concerned about potential disruptions in oil supply from crucial regions. The risk of a broader conflict involving Israel, its allies (such as the US, UK, and Saudi Arabia), and Iran, including its proxies like Hezbollah, poses a significant threat. Such a conflict could lead to substantial oil supply disruptions, driving up prices and contributing to increased production and transportation costs. This could result in a broader inflationary surge, impacting global economic stability, consumer spending, and growth. The situation is being monitored closely due to its potential inflationary risks.

Source: Bloomberg