September Update

Summary

The broader market response was mixed following the US Fed's 50 basis point rate cut in September, bringing the Fed Funds Rate to the range of 4.75%-5.00%. Initially, equities rallied on optimism that the rate reduction could stabilize a slowing economy. However, this was tempered by rising bond yields, as investors recalibrated expectations for further cuts, leaving markets divided over whether the Fed's move marked the start of a deeper easing cycle or a targeted measure to address labor market and inflation risks.

The U.S. dollar weakened against key currencies as traders anticipated additional rate cuts in 2024 and 2025. Safe-haven assets like gold surged on the prospect of prolonged lower yields, while oil prices held steady, reflecting concerns about global economic growth. Market sentiment remained cautious, with doubts over the Fed's ability to curb inflation without triggering a deeper economic slowdown.

At the same time, China's own stimulus measures injected a new dynamic into global markets. A combination of fiscal and monetary policies, including interest rate cuts and stock market support, temporarily buoyed Chinese equities. However, longer-term concerns persist over China's ability to overcome structural economic challenges, adding another layer of uncertainty to the global outlook.

Unexpected 50bps Hike: Is the Fed Lagging Behind the Market?

The Federal Reserve surprised the markets in September with a 50 basis point rate hike, a move that was viewed as aggressive despite being priced in by the futures market and bond yields. While many expected a 25bps cut, the Fed’s decision reflected growing concerns over strength of the labour market and its impact on long-term inflation control. Fed Chair Jerome Powell emphasized that this shouldn't signal a new norm, but with further cuts projected in 2024 and 2025, the Fed’s shift marks a dovish pivot from its July stance.

The Federal Reserve’s 2022-23 hiking cycle will be remembered for the highly unusual series of four consecutive 75 basis points interest rate increases. The cutting cycle initiated yesterday will be remembered for the highly unusual start of a 50 basis move. Both scenarios are widely viewed by commentators and market participants as indicators of the US central bank being late in its policy actions.

With the neutral rate around 3%, the US Fed and the market are showing vastly different timelines for achieving neutral rates. Market Overnight Index Swap (OIS) rates suggest hitting neutral rates by July next year, while bond pricing indicates we’ll reach it by the end of 2025. In contrast, the US Fed’s projections (dot plot) points to a target of neutral rates being acheived heading into the end of 2026. Despite the Fed implementing a steep 50 bps cut, the market still signals that the Fed is behind the curve.

Source: Bloomberg, Orestes Capital Management LLC

On average the S&P 500 rises 8.5% 18 months after the first Fed rate cut.

The Fed's actions are viewed as an "insurance policy" against a growing array of economic risks, even though the current economic landscape appears stable. Various motivations for the cut include concerns over potential recession, geopolitical tensions, and political pressures. By framing the rate cut as an insurance measure, the Fed signals its intent to proactively support against a new policy mistake, this time of being too tight for too long, and the belief of both the Fed and markets that the cost of this policy is very low.

Source: FactSet, Edward Jones

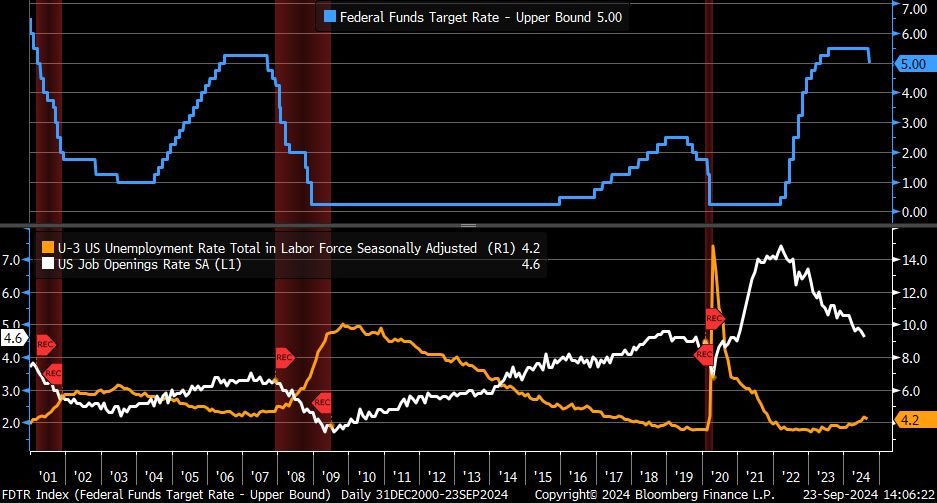

History Repeats? Monitoring Labor Market Stress After Fed's 50bps Rate Cut

Following the 50bps cuts that initiated Fed easing cycles in both 2001 and 2007, job openings and unemployment rates deteriorated rapidly. This swift downturn in the labour market underscored the challenges of timing monetary policy adjustments. As we look at today’s trends, it's important to monitor similar patterns. Job openings are already below their pre-pandemic highs, and the unemployment rate has been gradually rising. These converging trends could indicate potential stress in the labour market, mirroring past cycles where aggressive rate cuts were followed by economic slowdowns. If this pattern holds, further attention to these indicators is crucial as they may signal broader economic weakening ahead.

The risks facing markets have clearly shifted from inflationary pressures to concerns about economic growth. As a result, the focus has turned to the labor market, with monthly inflation data no longer posing the same level of risk as in recent years. However, this doesn't mean that a resurgence in inflation is off the table. We see a strong labor market as a potential driver of renewed inflationary pressures.

Source: Charles Schwab & Co., Inc.

Market now sees odds of recession by June 2025 50/50

The market is increasingly factoring in a recession as its base case scenario. Current Secured Overnight Financing Rate (SOFR) options suggest a strong likelihood of a hard landing, predicting a Federal Funds Rate of 3% or lower by next June, with a downturn now seen as having a 50% probability. However, this outlook appears overly pessimistic when considering the data, which indicates a low probability of recession in the coming three to four months. Analysts point to several economic indicators that do not support such a dire prediction.

Source: Bloomberg, Macrobond

Chinese Equities Experience Their Biggest One-Day Jump Since 2008 Amidst Stimulus Optimism

JPMorgan has highlighted China’s latest stimulus efforts as a response to the severity of its economic downturn, describing it as an emergency measure aimed at halting further decline rather than promoting sustained growth. The stimulus package includes key measures such as a 20-basis point cut to the seven-day reverse repo rate, a 50-basis point reduction in the reserve requirement ratio, and a $140 billion financial system injection. Additionally, the government allocated $113 billion to support the stock market, alongside initiatives to revitalize the struggling property sector through mortgage rate cuts and reduced down payments.

The immediate impact on China's stock market was striking. The Shanghai Composite Index surged 8.06%, its best single-day performance since 2008, contributing to a 17.39% gain for September. The Shenzhen Composite Index also posted a 10.9% increase, signaling a temporary boost in investor sentiment. However, despite this rally, the longer-term effectiveness of the stimulus is uncertain. Structural issues such as weak domestic consumption, unfavorable demographics, and diminished business confidence due to regulatory crackdowns remain unresolved. Trade barriers, particularly with the U.S. and Europe, further complicate China’s economic outlook. Investors remain cautious about whether the measures can truly address the deeper, persistent challenges facing the economy, such as deflationary pressures and volatile global demand.

Source: Bloomberg, JPAM